The Assemblée nationale adopted an amendment to the 2026 budget’s projet de loi de finances (PLF) on November 3. If it comes into law, the amendment will reduce the time required to be exempt from impôt sur la plus-value de cession by five years.

What are the current rules on capital gains on second homes in France?

Currently in France, homes that you use as your main residence are exempt from capital gains tax, regardless of the time between purchase and sale.

However, homes that are not your main residence are subject to capital gains tax, if less than 22 years have passed between purchase and sale.

After 22 years, owners are 100% exempt from capital gains tax, but must still pay social charges if the property is sold during the 23rd to 30th year of ownership. If the property is sold after 30 years, owners are exempt from 100% of capital gains and social charges.

The taxes due benefit from an abatement, or reduction, per year of ownership. (If passed, the new amendment would reduce the year of exemption from 22 years to 17.)

The current abatement rules are:

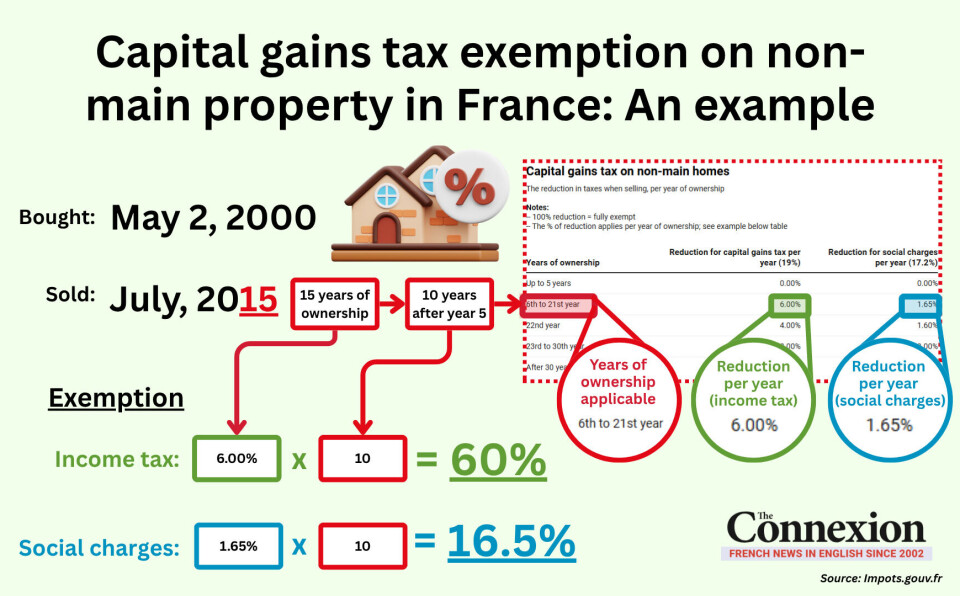

Capital gains: An example

How to calculate capital gains and social chargesConnexionFrance / Impots.gouv.fr / Canva

An example (from the French tax website) explains how it would work for an apartment purchased on May 2, 2000.

Advertisement

If the apartment was sold in July 2015, this would mean it qualifies for the rate reductions applying to a sale 15 years after purchase. This means:

The sale is taking place in the ‘6th to 21st year of ownership’ bracket

Income tax is therefore charged at 6%

The 6% is multiplied by 10, for 10 years of ownership beyond the fifth year

Social charges are charged at 1.65%

The 1.65% is also multiplied by 10, for 10 years of ownership beyond the fifth year

This means it would benefit from a tax allowance of:

60% for income tax (6% x 10 years)

16.5% for social security charges (1.65% x 10 years).

The property would become fully exempt from income tax on May 2, 2022 (2000 + 22 years) and from social security charges on May 2, 2030 (2000 + 30 years).

The French tax authorities have a phone helpline that can help with this issue, if needed. It is 0809 401 401 from within France, open weekdays from 08:30 to 19:00 (the service is free but the call itself is subject to normal phone charges).

Those living outside of France can call the non-resident line on + 33 1 72 95 20 42.